It’s incumbent upon me, as your tech columnist, to keep you apprised of the latest. I covered useful services such as Amazon and Google when they launched, and we’ve looked at interesting and seemingly important developments such as Bitcoin, cryptocurrency, blockchain, and the metaverse.

Now it’s time to take a look at NFTs. And, frankly, your columnist hasn’t a clue.

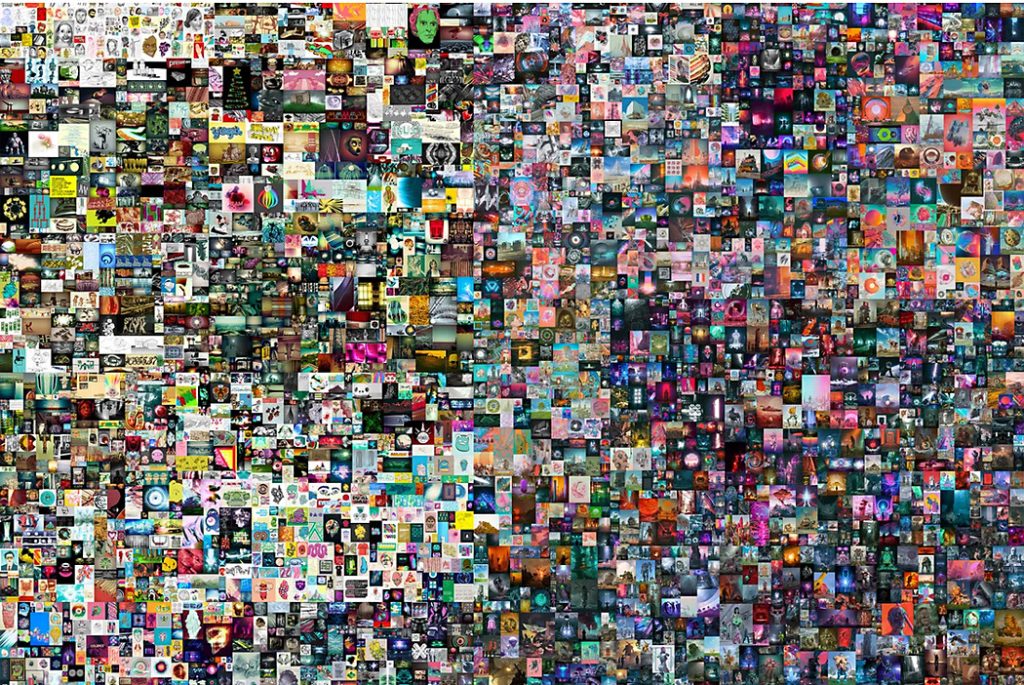

Let’s start with Beeple, otherwise known as Mike Winkelmann. He’s well-known in the world of digital art. For 14 years, he’s been creating a daily digital artwork. In March of last year, he collected all these pieces into a digital collage and auctioned it off via Christie’s in the UK. It sold for $69 million.

And what did the happy winner of the auction receive? An NFT. Which is simply an entry in a blockchain that indicates he owns this work.

He didn’t take possession of the work itself, which only exists digitally. Perhaps he has a copy on his computer, but so do I. And you, too, could download it to your computer, if you like. Just Google Everydays: the First 5000 Days.

Would you spend $69 million for an entry in a blockchain indicating you are the owner of a digital work of art? I can think of other ways I’d spend that money.

Why would someone do it? One answer typically given is that it’s an investment and the person expects the value to increase.

There are precedents. In October of 2020 Beeple auctioned his first NFTs, with a pair of them going for $66,000. One of those NFTs was resold for $6.6 million.

Okay, Jim, don’t be coy. Just what is an NFT? It stands for non-fungible token. Now you understand, right?

This is in contrast to fungible tokens, such as Bitcoin. That means that Bitcoins can be substituted for one another, like money, and can be used for monetary transactions. Non-fungible means the tokens are unique.

Common types of NFTs include digital art, music, sports video clips, and much more.

The first NFTs appeared as colored tokens on the Bitcoin blockchain in 2014, but the market didn’t take off until the Ethereum cryptocurrency launched in 2015. This platform included a set of standards that developers could use to create tokens to be stored in Ethereum’s underlying blockchain.

Okay, Jim, don’t be coy. Just what, again, is a blockchain? This is simply a public ledger stored on computers that are part of a cryptocurrency network, such as the computers that “mine” Bitcoin.

The beauty of a blockchain is that it is decentralized. Every node on the network has the entire blockchain record of transactions, and every transaction goes through a strict process of verification. This decentralization makes it nearly impossible to cheat. And it lies completely outside any central control, whether government or corporate.

Many people are now referring to blockchain technologies, including NFTs, as internet 3.0. (Internet 1.0 was Google, etc.; 2.0 was social media.) Tech executives are fleeing their multimillion-dollar salaries to join blockchain startups, sensing this is the next big thing.

If you think $69 million for a blockchain entry signifying ownership is bizarre, it gets even weirder. In my November column, we looked at the imminent “metaverse” championed by Facebook founder Mark Zuckerberg and others—a digital realm that we’ll inhabit.

Zuckerberg envisions a social environment like Facebook, but with virtual cities and bowling alleys and movie theaters and concert halls where we’ll get together with the digital representations of friends.

Startups are rapidly creating digital cities and selling property in them. Decentraland, for example, has created a digital realm with 90,000 parcels of “land.” Last November, Tokens.com purchased “land” in Decentraland’s fashion district for about $2.5 million, convinced it was an excellent investment for a parcel in the downtown core. (In other words, location, location, location.)

That purchase, of course, was paid for with cryptocurrency and recorded as an NFT in a blockchain. NFT technology will also facilitate metaverse purchases such as artwork, music, and homes.

Your tech columnist can’t quite get his head around this.

Okay, Jim. Don’t be coy. Many believe that NFTs can actually be quite useful.

According to Investopedia, tokenizing real-world assets, such as real estate, “allows them to be bought, sold, and traded more efficiently while reducing the probability of fraud.” And some voting experts say that NFTs are an ideal technology for voting. It would ensure that you are eligible to vote (by giving you a unique entry in a blockchain), make it impossible to vote twice, and hugely facilitate tabulation of votes.

This technology could also be useful in recording supply-chain transactions. For example, extensive fraud has been documented in the organic food industry. If all the transactions of a load of grain were available in a public ledger, it would be easier for distributors and manufacturers to track authenticity.

Still, I wouldn’t spend $69 million on a digital art NFT.

Find column archives at JimKarpen.com.